The Ultimate New Tax Regime Guide: FY 2024-25, FY 2026-27 & FY 2027-28

The landscape of direct taxation in India has transitioned rapidly towards simplification. Through consecutive union budgets, the Indian government has structured the **New Tax Regime** to become the default tax system for individual taxpayers. By offering lower slab rates and wider tax brackets, the regime seeks to provide direct tax relief to the middle class without requiring them to lock up their liquidity in long-term financial instruments like public provident funds (PPF), equity-linked savings schemes (ELSS), or multi-year life insurance plans.

To assist taxpayers in planning their salary packages and structuring their corporate perks, this guide details the exact slab differences across **FY 2024-25 (AY 2025-26)**, **FY 2026-27 (AY 2027-28)**, and **FY 2027-28 (AY 2028-29)**. We analyze key corporate benefits—such as Employer NPS shares and Sodexo meal allowances—and provide side-by-side tax computation examples to help you optimize your tax planning.

Multi-Year Slab Comparison: Budget 2024 vs. Budget 2026 Slabs

Under the New Tax Regime, the progressive slabs undergo changes to offer higher tax-free thresholds. Below is the side-by-side comparison of the tax brackets for the financial years covered:

| Taxable Income Bracket | Rate |

|---|---|

| Up to ₹3,00,000 | 0% |

| ₹3,00,001 to ₹7,00,000 | 5% |

| ₹7,00,001 to ₹10,00,000 | 10% |

| ₹10,00,001 to ₹12,00,000 | 15% |

| ₹12,00,001 to ₹15,00,000 | 20% |

| Above ₹15,00,000 | 30% |

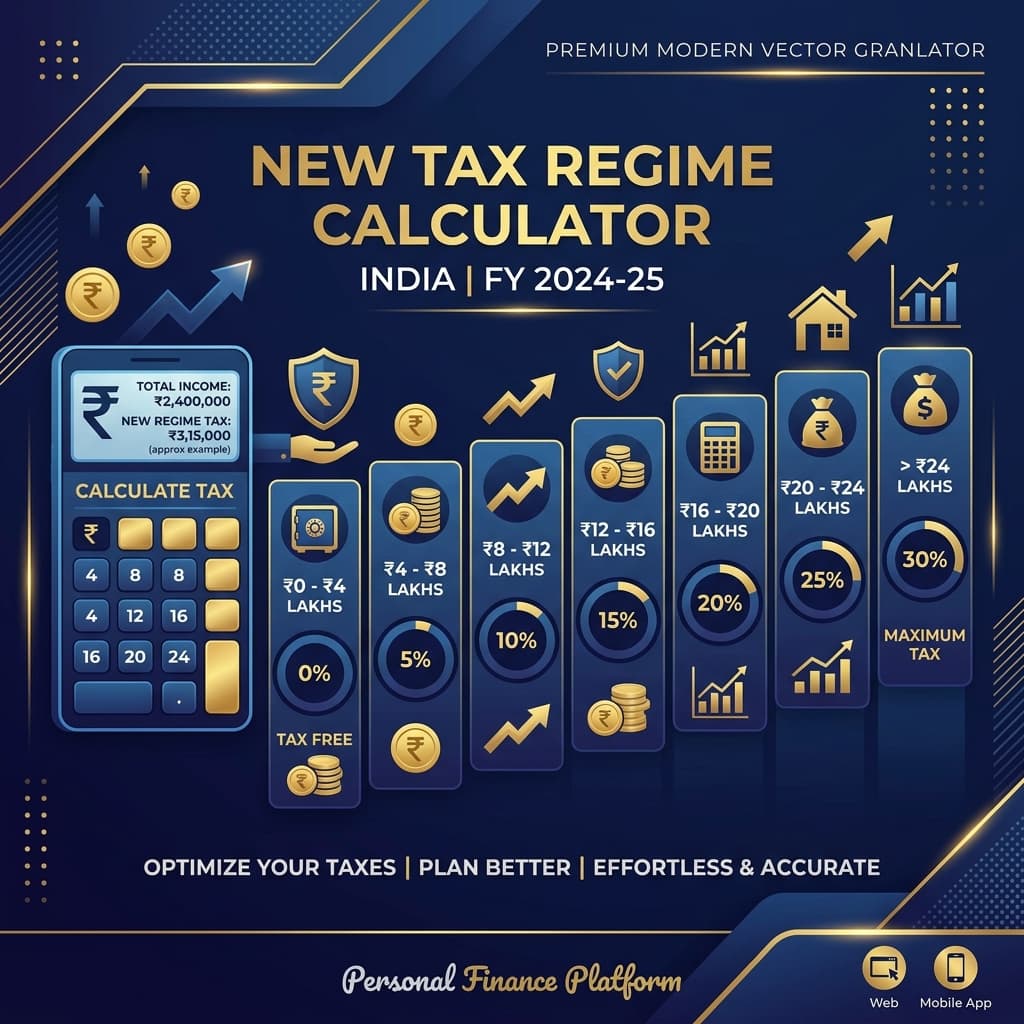

| Taxable Income Bracket | Rate |

|---|---|

| Up to ₹4,00,000 | 0% |

| ₹4,00,001 to ₹8,00,000 | 5% |

| ₹8,00,001 to ₹12,00,000 | 10% |

| ₹12,00,001 to ₹16,00,000 | 15% |

| ₹16,00,001 to ₹20,00,000 | 20% |

| ₹20,00,001 to ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Starting from FY 2026-27, the initial zero-tax bracket has been expanded from ₹3 Lakhs to ₹4 Lakhs, and the progressive slabs are stretched in ₹4 Lakh intervals rather than the older ₹3 Lakh/₹2 Lakh intervals. This expansion reduces the tax burden on middle-income groups.

The Standard Deduction: A Flat ₹75,000 Exemption

For all salaried workers and pensioners, a flat **standard deduction of ₹75,000** is available across all three financial years (FY 2024-25, FY 2026-27, and FY 2027-28) under the New Tax Regime. In July 2024, the government increased the standard deduction from ₹50,000 to ₹75,000 to provide direct tax relief.

This deduction is subtracted directly from your gross CTC at source by your employer's payroll team. Because it is a standard deduction, it requires no proof of savings, house rent receipts, or lock-in contributions. It simply reduces your gross CTC by ₹75,000 instantly.

Section 87A Rebate and Marginal Relief

The Section 87A rebate serves as the primary tax relief mechanism for lower and middle-income groups under the New Tax Regime. By applying a rebate, the tax liability is reduced to zero if the net taxable income remains below a specific threshold:

- FY 2024-25 (AY 2025-26): The Section 87A rebate covers taxable incomes up to **₹7,00,000**. The maximum rebate available is **₹20,000**. Adding the standard deduction of ₹75,000, any salaried employee earning a gross CTC of up to ₹7.75 Lakhs pays ₹0 tax.

- FY 2026-27 & FY 2027-28: The Section 87A rebate threshold is raised to **₹12,00,000**. The maximum rebate increases to **₹60,000**. Combined with the ₹75,000 standard deduction, a salaried employee with a gross CTC of up to ₹12.75 Lakhs pays ₹0 tax.

The Role of Marginal Relief:

Marginal relief is designed to resolve a tax cliff where earning slightly more than the rebate limit triggers a full slab tax liability. Without relief in FY 2024-25, earning ₹7,05,000 taxable income would trigger a slab tax of ₹20,250. Marginal relief limits the tax to the excess income earned over the threshold (e.g. ₹5,000), saving the taxpayer from a disproportionate tax penalty.

Exempt Allowances: NPS Employer Share & Meal Cards

Under the New Tax Regime, you cannot deduct HRA or Section 80C investments, but there are valuable exemptions that you can utilize through corporate CTC restructuring:

Employer NPS Contribution (Section 80CCD(2))

Starting FY 2024-25, the corporate deduction for employer contributions to the National Pension System (NPS) under Section 80CCD(2) has been standardized. Salaried employees in both private sector companies and public/government undertakings can claim a deduction up to **14% of their Basic salary + DA**. This provides a direct path to lower taxable income through salary structuring.

Tax-Exempt Meal Vouchers

Meal vouchers (food cards or paper coupons) are exempt from income tax up to **₹200 per meal, for up to two meals per working day** (a total of ₹400 per working day). For a standard calendar year with 22 working days per month, this translates to **₹8,800 monthly** or **₹1,05,600 annually** in tax-free benefits. Restructuring a portion of your monthly allowances into meal cards directly reduces your taxable CTC.

Side-by-Side Example: Gross CTC of ₹15 Lakhs

To illustrate the tax changes over time, let's examine the tax liability for a salaried employee with a gross CTC of **₹15,00,000** (assuming no deductions other than the ₹75,000 standard deduction):

// FY 2024-25 (AY 2025-26)

Gross Annual CTC: ₹15,00,000

Less: Standard Ded.: -₹75,000

Net Taxable Income: ₹14,25,000

// Progressive Tax Math:

- Up to ₹3L @ 0%: ₹0

- ₹3L to ₹7L @ 5%: ₹20,000

- ₹7L to ₹10L @ 10%: ₹30,000

- ₹10L to ₹12L @ 15%: ₹30,000

- ₹12L to ₹14.25L @ 20%: ₹45,000

Total Slab Tax: ₹1,25,000

Add: Education Cess (4%): ₹5,000

Net Tax Liability: ₹1,30,000

// FY 2026-27 & FY 2027-28

Gross Annual CTC: ₹15,00,000

Less: Standard Ded.: -₹75,000

Net Taxable Income: ₹14,25,000

// Progressive Tax Math:

- Up to ₹4L @ 0%: ₹0

- ₹4L to ₹8L @ 5%: ₹20,000

- ₹8L to ₹12L @ 10%: ₹40,000

- ₹12L to ₹14.25L @ 15%: ₹33,750

Total Slab Tax: ₹93,750

Add: Education Cess (4%): ₹3,750

Net Tax Liability: ₹97,500

Comparing the two periods shows that the expanded slabs in FY 2026-27 reduce the net tax liability for a ₹15 Lakh income from **₹1,30,000** to **₹97,500**. This delivers a direct tax saving of **₹32,500** annually, lowering the effective tax rate on a ₹15 Lakh income to just **6.5%**.