Home Loan Eligibility Calculator 2026: Estimate Your Borrowing Capacity

Determine your maximum home loan eligibility under Indian banking standards using the Fixed Obligations to Income Ratio (FOIR) model. Assess co-applicants offsets and model dynamic amortization structures.

FOIR Ceiling Limits

Banks restrict monthly obligations to 40%-60% of income. Reducing personal loans expands home loan eligibility.

Interest Rate Leverage

Lower interest rates drop monthly EMIs, directly boosting the maximum principal amount you can borrow.

Tenure Extension

Extending the loan tenure to 20 or 30 years spreads out principal repayments, increasing your immediate borrowing cap.

Borrowing Capacity Modeler

Mortgage Eligibility Modeler

Fast & Precise FOIR Calculation

Ultimate Guide to Home Loan Eligibility in India

Owning a house is a significant milestone for families and professionals in India. However, because real estate purchases require substantial capital, buying a home is almost always paired with a long-term mortgage. Before you begin scouting properties or selecting interior designs, the absolute first step is to answer a critical financial question: How much home loan can I qualify for?

A Home Loan Eligibility Calculator 2026 helps clear this ambiguity. By evaluating variables such as your gross salary, interest rates, tenure, co-applicant additions, and existing liabilities (such as car or personal loan EMIs), this tool models the exact criteria used by banks like HDFC, SBI, Axis, and ICICI to decide your credit limit. This comprehensive guide details the calculations, variables, and strategies you can use to maximize your eligibility.

1. How Banks Determine Your Home Loan Eligibility: The FOIR Model

In India, financial institutions evaluate home loan eligibility using the **FOIR (Fixed Obligations to Income Ratio)** method. This ratio determines the portion of your net monthly income that can be comfortably used to pay off debts, including existing EMIs and your new home loan.

Banks want to ensure you have enough remaining income to cover living expenses, household groceries, children's education, and insurance premiums. Therefore, they set strict FOIR ceilings based on your total income levels:

- Total Income < ₹30,000: The maximum permissible debt obligation is limited to 40% of income.

- Total Income ₹30,000 to ₹50,000: The permissible debt obligation limit rises to 50%.

- Total Income ₹50,000 to ₹1,00,000: The limit increases to 55%.

- Total Income > ₹1,00,000: High-income earners can dedicate up to 60% of their earnings to debt repayment.

For example, if your net monthly household income is ₹75,000, your FOIR threshold is 55%. This means your total monthly EMI obligations (existing loans + new home loan) cannot exceed ₹41,250.

2. The Mathematics: How Your Loan Amount is Calculated

Once the bank calculates your maximum permissible home loan EMI, it uses standard compound interest math to work backward and find your borrowing limit:

Step 1: Calculate Maximum Permissible New EMI

Max New EMI = (Total Net Monthly Income × FOIR Limit Ratio) - Existing EMIs

Step 2: Calculate Maximum Eligible Principal (P)

Using the amortization formula:

Eligible Principal = Max New EMI × [ (1 + r)^n - 1 ] ÷ [ r × (1 + r)^n ]

Where:r = Monthly interest rate (Annual rate ÷ 12 ÷ 100)n = Total months (Tenure in years × 12)

3. The LTV (Loan to Value) Ratio Factor

Even if your income permits a ₹1 Crore loan, banks will never fund the entire cost of the property. The **LTV (Loan to Value) Ratio** restricts the maximum loan amount based on the actual market value of the property:

- Property Value up to ₹30 Lakhs: Maximum LTV ratio allowed is up to 90% (requiring a 10% down payment).

- Property Value ₹30 Lakhs to ₹75 Lakhs: Maximum LTV ratio allowed is up to 80% (requiring a 20% down payment).

- Property Value above ₹75 Lakhs: Maximum LTV ratio allowed is up to 75% (requiring a 25% down payment).

This means buyers must have enough personal savings to cover the remaining down payment, registration fees, stamp duty, and brokerage fees.

4. Key Factors Influencing Home Loan Eligibility

When reviewing your mortgage application, lenders look at several factors to evaluate risk:

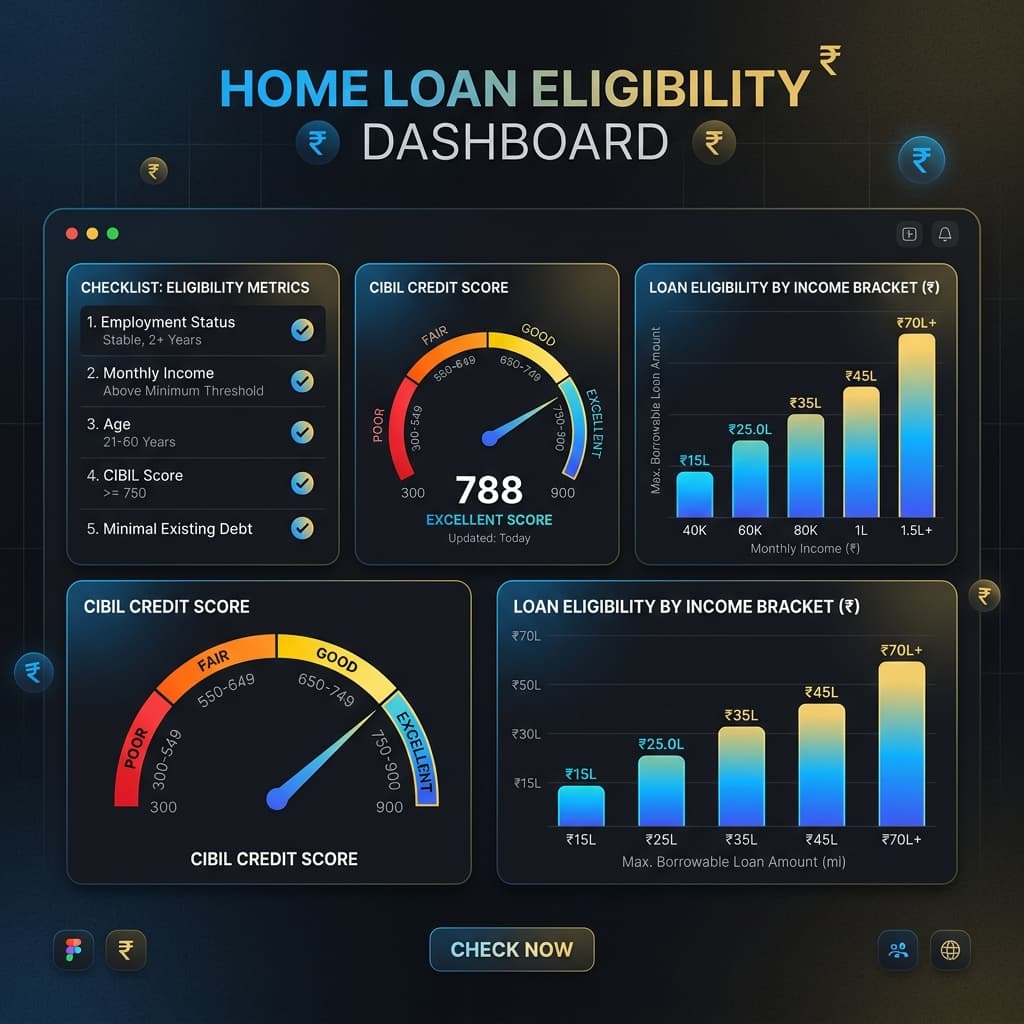

- CIBIL Score: A CIBIL score of 750 or higher is ideal. It signals disciplined credit history and allows you to secure the lowest interest rates, increasing your overall borrowing power.

- Age of Applicant: Younger applicants (25-35 years) can secure longer loan tenures of up to 30 years. Older applicants closer to retirement are offered shorter tenures, lowering their eligibility.

- Nature of Employment: Salaried employees working in blue-chip MNCs or government agencies are viewed as low-risk, securing smoother loan approvals compared to self-employed individuals with variable incomes.

- Location and Legality of Property: Banks thoroughly audit the property builder, municipal approvals (RERA registration), and property age before dispersing the loan.

5. How to Increase Your Home Loan Eligibility

If your calculated eligibility is lower than the price of your target home, consider these effective strategies to boost your borrowing limit:

- Add a Co-applicant: Apply for a joint home loan with a working spouse, parent, or sibling. Combining incomes increases your eligible borrowing limit.

- Clear Existing High-Interest Debts: Pay off outstanding credit card balances, personal loans, or car loans before applying. This lowers your existing EMIs, increasing your FOIR buffer.

- Opt for a Longer Tenure: Extending your tenure from 15 to 25 or 30 years reduces your monthly EMI, which helps you qualify for a larger principal amount.

- Declare Additional Income Sources: Provide evidence of rental income, annual bonuses, or dividend payments to raise your total monthly income base.

Frequently Asked Questions (FAQs)

What is FOIR and how does it determine my home loan eligibility?

FOIR stands for Fixed Obligations to Income Ratio. It is the percentage of your monthly income that banks allow you to spend on loan repayments (such as existing credit card or car loan EMIs, plus your new home loan). Typically, banks cap FOIR between 40% and 60% depending on your monthly income.

Can a joint home loan increase my borrowing capacity?

Yes. Applying for a joint home loan with a co-applicant (such as your spouse, parent, or working sibling) combines your incomes, raising the total monthly income base. This increases your permissible monthly EMI limit and boosts your eligibility.

How does my CIBIL score affect my eligibility?

A CIBIL score of 750 or above is ideal. A high credit score signals to lenders that you are a low-risk borrower, helping you secure lower interest rates. Lower interest rates reduce your monthly EMI, which directly increases the maximum loan amount you can qualify for.

What is the LTV ratio and how does it impact down payments?

LTV (Loan to Value) ratio is the percentage of the property value that banks are willing to finance. For properties valued under ₹30 Lakhs, banks may fund up to 90% (requiring a 10% down payment). For properties above ₹75 Lakhs, the LTV is capped at 75% (requiring a 25% down payment).

Does choosing a longer loan tenure increase eligibility?

Yes. A longer tenure (such as 25 or 30 years) spreads the principal repayment over more months, which reduces the monthly EMI. A lower EMI helps you qualify for a larger loan amount under your income constraints.

Can I get a home loan if I have an outstanding car or personal loan?

Yes, but your eligibility will be reduced. Banks subtract your existing monthly EMIs from your permissible FOIR debt limit. The remaining balance is the maximum EMI you can pay for your new home loan, which lowers the maximum principal amount you can borrow.

Are there tax benefits on home loans in India?

Yes. Under Section 24(b) of the Income Tax Act, you can claim deductions of up to ₹2 Lakhs per year on the interest paid for a self-occupied home. Additionally, under Section 80C, you can claim deductions of up to ₹1.5 Lakhs per year on the principal repayment amount.

How do banks treat variable income like bonuses or commissions?

Banks typically take a 2-to-3-year average of your variable income (such as incentives, commissions, or annual performance bonuses) to ensure it is stable, and then add it to your gross monthly income base.

Rohit Kushwaha

Software Engineer & Creator of mysalarycalculator.in

I'm Rohit Kushwaha, a Software Engineer with 3+ years of experience in developing web applications and digital solutions. By combining technology with practical financial tools, I built mysalarycalculator.in to help Indian professionals easily understand their salary, taxes, EPF, gratuity, and take-home income.

Comments & Discussion (0)

Join the Conversation

No comments yet. Be the first to start the discussion!