Interest-Free Home Loan Calculator 2026: SIP Offset Strategy

Learn how to make your home loan effectively interest-free by running a parallel SIP investment. Enter your loan details and see how much to invest monthly to accumulate a corpus that completely offsets your interest.

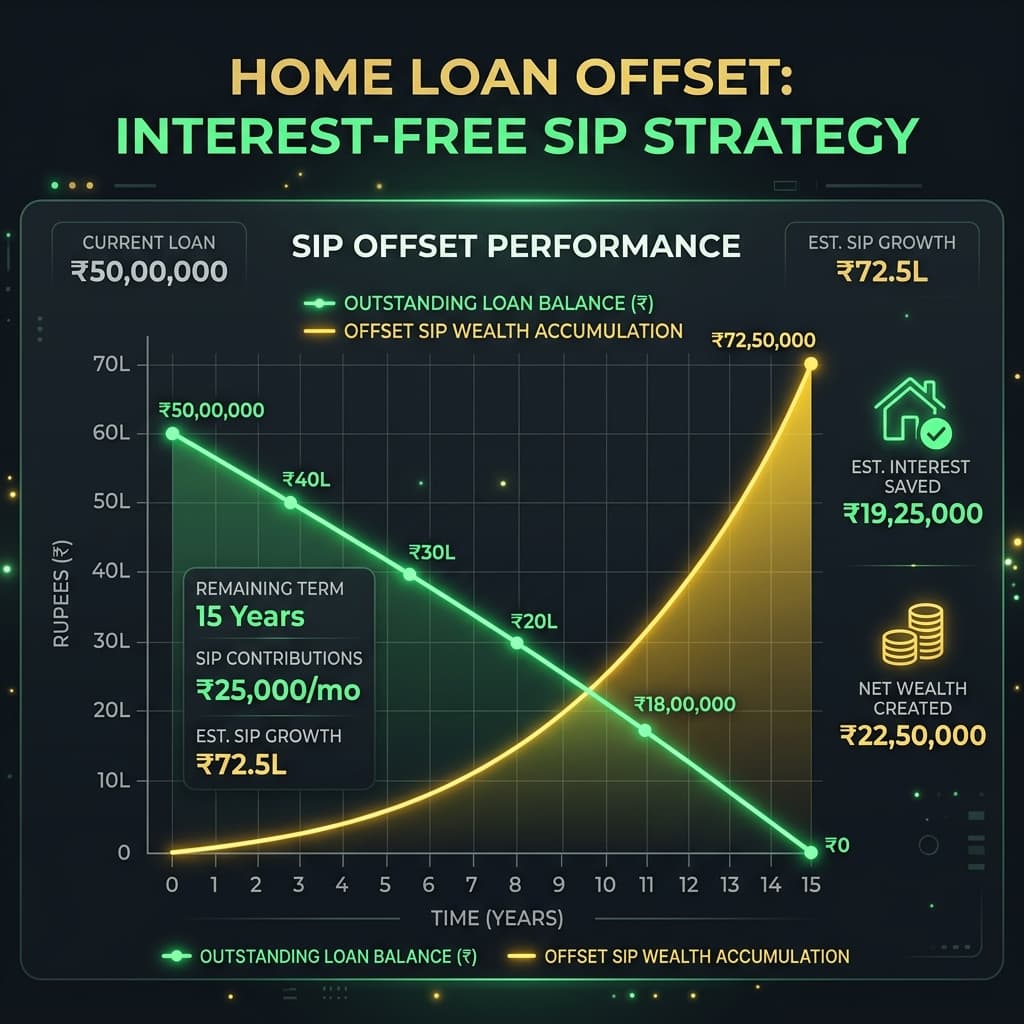

Compounding Power

Leverage long home loan tenures (15-30 years) to let equity mutual fund SIPs compound and grow into a massive offset corpus.

Effective Offset

A minor parallel investment (typically 12% of your EMI) is sufficient to generate returns matching your total loan interest.

Wealth Creation

Instead of losing money to bank interest, you exit the tenure with the property and your entire interest recovered as investment growth.

Interest-Free Calculator & Strategy Simulator

Home Loan + SIP Optimizer

Set up your parallel plan to offset home loan interest payouts

Latest Indian Home Loan Rates (2026 Reference)

Use these representative rates from leading financial institutions in India to configure your simulator accurately. Actual rates fluctuate based on credit score, loan size, and gender.

| Lending Institution | Interest Rates (p.a.) | Processing Charges |

|---|---|---|

| Union Bank of India | 8.35% - 10.75% | Nil to 0.50% (Max ₹10,000) |

| State Bank of India (SBI) | 8.40% - 10.15% | Nil to 0.35% (Min ₹2,000, Max ₹10,000) |

| HDFC Bank | 8.50% - 9.85% | Up to 0.50% of loan amount (Min ₹3,000) |

| Bank of Baroda | 8.40% - 10.60% | Nil to 0.50% (Max ₹15,000) |

| ICICI Bank | 8.75% - 9.65% | Up to 0.50% of loan amount (Min ₹3,000) |

| Axis Bank | 8.75% - 9.60% | Up to 1.00% of loan amount (Min ₹10,000) |

Interest-Free Home Loans: The Ultimate Guide to the SIP Offset Strategy

For a vast majority of Indian households, buying a house is the single largest financial transaction they will ever make. Because property prices in urban centers have skyrocketed, it is virtually impossible to buy a home without seeking external financing. Home loans are the primary vehicle for achieving this milestone. However, they come with a hefty catch: over a 15, 20, or 30-year tenure, the compounding interest you pay to the bank can easily match or even exceed the original principal borrowed.

Imagine borrowing ₹50 Lakhs from a bank, only to pay back more than ₹1 Crore by the end of the term. The thought of losing ₹54 Lakhs solely in interest can be financially draining. But what if there was a way to legally and strategically recover every single rupee paid as interest?

This is where the **Interest-Free Home Loan Strategy** (often called the **Parallel SIP Offset Strategy**) comes into play. By combining a standard home loan with a disciplined monthly Systematic Investment Plan (SIP) in diversified equity mutual funds, you can build an parallel asset that compounds rapidly. At the end of the loan tenure, the profits from your SIP will match the total interest paid to the bank, rendering your home loan effectively interest-free.

1. The Mathematics Behind the Strategy

To understand how this strategy functions, we must look at the mathematical engines driving both sides of the balance sheet: **reducing-balance loan interest** (which works against you) and **compounded SIP returns** (which work for you).

When you take a home loan, the bank calculates your monthly EMI using the standard formula:

EMI = P × r × [ (1 + r)^n ] / [ (1 + r)^n - 1 ]

Where:

• P = Principal amount (e.g., ₹50 Lakhs)

• r = Monthly interest rate (Annual Rate / 12 / 100)

• n = Total number of monthly installments (Years × 12)

Because home loans use a reducing balance calculation, interest is computed on the outstanding balance at the end of each month. In the early years, since the outstanding balance is high, the interest portion consumes the majority of your EMI. Over a long tenure like 20 years, a loan of ₹50 Lakhs at 8.5% interest results in a monthly EMI of ₹43,473. By the end of 240 months, you will have paid ₹1,04,33,520 in total, consisting of the ₹50 Lakhs principal and **₹54,33,520 in interest**.

To neutralize this interest component, we start a parallel monthly SIP. The future value (FV) of an annuity due (invested at the beginning of each month) is calculated using the formula:

FV = PMT × [ ((1 + i)^n - 1) / i ] × (1 + i)

Where:

• PMT = Monthly SIP contribution

• i = Monthly expected SIP return rate (Annual return / 12 / 100)

• n = Number of compounding periods (Months)

If we expect our mutual fund portfolio to generate a conservative return of 12% p.a., the compounding factor over 20 years is massive. By plugging ₹54,33,520 as the target Future Value into this equation, we find that the required monthly SIP is only **₹5,438**.

Let us analyze the cash flows:

- Total out-of-pocket investment in SIP: ₹5,438 × 240 months = ₹13,05,120

- Total capital growth generated by market: ₹54,33,520 (Corpus) - ₹13,05,120 (Investment) = ₹41,28,400

- Total loan interest paid to bank: ₹54,33,520

- Net Interest Cost: ₹54,33,520 (Paid) - ₹54,33,520 (Recovered from SIP) = **₹0**

Your actual net outflow throughout the strategy is simply the loan principal (₹50 Lakhs) and your SIP investments (₹13.05 Lakhs), totaling ₹63.05 Lakhs. Without the SIP, your net outflow would have been ₹1.04 Crores. Compounding has literally saved you over ₹41 Lakhs in interest!

2. Core Rules of Thumb for Home Buyers

If the detailed formulas seem complex, financial planners in India generally recommend two simple thumb rules for executing this strategy:

- The 10% EMI Rule: Start a parallel monthly equity mutual fund SIP equal to exactly 10% of your home loan EMI. For instance, if your EMI is ₹50,000, start a parallel SIP of ₹5,000. Over 20 years, assuming a typical 12% to 15% return, this SIP will yield a corpus that recovers almost 80% to 100% of your interest.

- The 0.1% Principal Rule: Set your monthly SIP to 0.1% of the total loan principal. For a ₹50 Lakh loan, this translates to ₹5,000 per month (0.1% of ₹50,00,000). This rule ensures that your SIP is aggressively funded from day one, giving you a high margin of safety against market volatility.

3. Crucial Risks and Reality Check

While the math on paper is flawless, it is imperative to remember that **this is a financial strategy, not a magic trick**. Real-world execution comes with significant variables:

- Debt is Guaranteed, Returns are Probabilistic: Your home loan EMI is a contractually binding liability. If interest rates rise, the bank will increase your tenure or EMI. On the other hand, equity mutual fund returns are volatile. A long-term average of 12% is highly possible based on historical performance, but you could experience prolonged periods of flat or negative returns.

- Liquidity & discipline: Servicing both a home loan EMI and a monthly SIP requires significant, consistent cash flow. In times of job loss or business downturns, maintaining both payouts can cause cash flow stress.

- Inflationary Impact: While the SIP corpus matches the interest paid, the purchasing power of that money will have decreased due to inflation over 20 years. However, this is still vastly superior to having no offset corpus at all.

4. Tax Considerations and Regulations (FY 2026-27)

To evaluate the net benefits of this strategy, you must factor in the taxation rules under the Indian Income Tax Act:

- Home Loan Tax Benefits (Old Tax Regime): Under Section 24(b), you can claim deductions of up to ₹2 Lakhs per year on interest paid for self-occupied homes. Under Section 80C, principal repayments up to ₹1.5 Lakhs are tax-deductible. If you choose the Old Tax Regime, these deductions reduce your effective interest rate.

- New Tax Regime Limitations: Under the New Tax Regime (which is the default for FY 2026-27), deductions under Section 80C and Section 24(b) for self-occupied properties are not available. This makes the interest load heavier, making the SIP offset strategy even more critical.

- Mutual Fund Capital Gains Tax: Equity mutual fund gains are classified as Long-Term Capital Gains (LTCG) if held for more than 12 months. Starting FY 2024-25 and continuing into 2026, LTCG on equity mutual funds is taxed at **12.5%** on gains exceeding ₹1.25 Lakhs in a financial year. To achieve a true interest-free offset, you should increase your SIP target by 10% to account for this tax liability at withdrawal.

5. How to Optimize and Accelerate the Strategy

If you want to maximize the efficiency of your offset strategy, consider implementing these professional optimization techniques:

- Utilize a Step-Up SIP: Do not keep your SIP contribution constant for 20 years. As your income increases, step up your monthly SIP amount by 5% or 10% every year. A 10% annual step-up can double your final corpus or slash the time required to offset your interest in half (from 20 years to 11-12 years).

- Asset Allocation Shift: During the first 15 years of your 20-year term, invest your SIP heavily in equity mutual funds (large-cap, multi-cap, or index funds) to capture high growth. In the final 3-5 years, gradually move your accumulated SIP corpus into safer debt funds or arbitrage funds via a Systematic Transfer Plan (STP) to lock in gains and prevent late-tenure market crashes from eroding your corpus.

- Combine with Home Loan Prepayments: If you receive annual bonuses, use them to make principal prepayments directly to your home loan. Prepaying even 1 or 2 extra EMIs per year, combined with a parallel SIP, creates a double-whammy effect that destroys debt rapidly while keeping your wealth-creation engine running.

Frequently Asked Questions (FAQs)

Rohit Kushwaha

Software Engineer & Creator of mysalarycalculator.in

I'm Rohit Kushwaha, a Software Engineer with 3+ years of experience in developing web applications and digital solutions. By combining technology with practical financial tools, I built mysalarycalculator.in to help Indian professionals easily understand their salary, taxes, EPF, gratuity, and take-home income.

Comments & Discussion (0)

Join the Conversation

No comments yet. Be the first to start the discussion!